This was a 3-4 hour unpaid interview task. The foundation was formed but nothing here is production-ready. Here’s what I am / am not delivering:

✅ Problem & approach definition

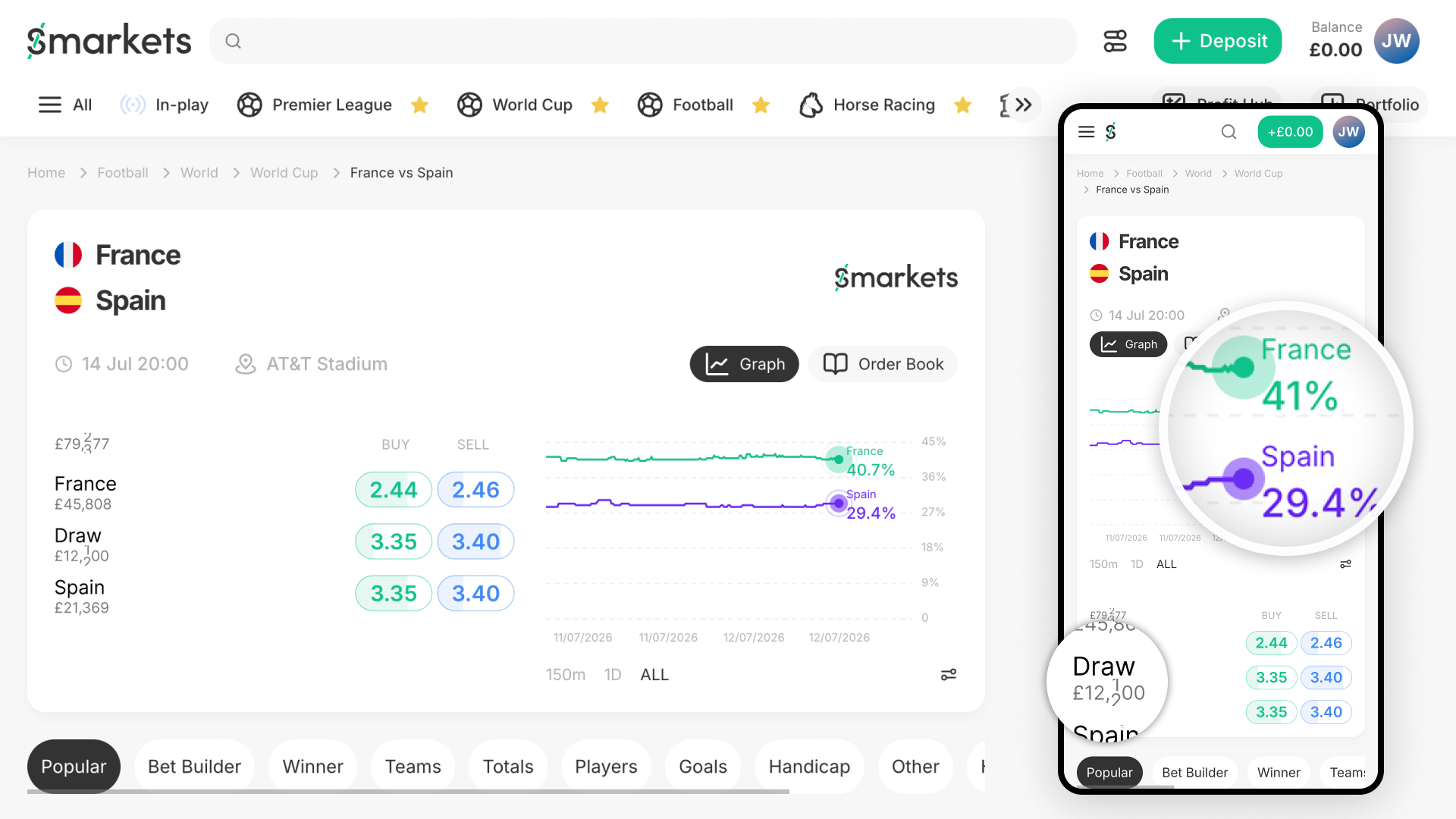

✅ Single-state UI mockups

✅ Action plan

❌ Vibe coded prototype

❌ User journeys

❌ Component breakdowns

❌ Active animations